ELDER LAW SERVICES OF CALIFORNIA:

ELDER-CARE, MEDI-CAL

How do I plan for elder care for my parents or myself? How can we make sure that we won’t outlive our money? How do we go about estate planning, including a living trust, legal and medical powers of attorney? Are there any particular elder law California planning requirements? Can I protect my house from Medi-Cal recovery? We take a typical elder-care journey with Ann, age 80, and her daughter Jean who sought out the elder law services of California attorneys.

By James L. Cunningham Jr., Esq.

Like any endeavor, successful aging with elder law takes planning—not just by seniors themselves, but by those who love them. Unfortunately, far too few Americans do the advanced work to deal with the inevitable issues that arise with age.

This lack of planning comes not just from our natural reluctance to deal with difficult issues until they arise, but because few of us have the necessary legal and financial expertise to make the right moves. For most, the first time dealing with elder-care issues in America is like arriving as a “stranger in a strange land.” You simply don’t know the landscape. And worse, you don’t know what you don’t know.

At our firm, we believe that people need and deserve qualified guides through the many obstacles in handling—and paying for—aging. The legal and financial issues are real, they’re pressing, and we know from daily experience that professional advice and legal support prevent real disasters for families. Click here to book a free call with a client specialist.

Let’s look at some of the legal and financial issues of elder care through which we guide families every single day.

We’ll follow Ann, age 80, through a typical journey late in life. But first, let me set up a little roadmap.

Elder-Care Planning Stages

As I see it, there are three stages of elder-care planning:

- Pre-Planning before an incapacity

- Non-Crisis Planning after a diagnosis, but before mental incapacity

- Crisis Planning

Here’s a hard truth: Much of Pre-Planning, including Estate Planning, can only occur when parents are of sound mind. It is simply impossible for many financial and legal arrangements to be made after someone is mentally incapacitated or has passed away. Many people do not know this hard truth, and the result is often catastrophic—not just years in court, but tens of thousands or millions of dollars lost. I cannot tell you how many clients come to me when their parents have passed, and ask, “They never created a Will or Trust. Can I create one for them now?” The answer, unfortunately, is no.

The next phase, Non-Crisis Planning, generally begins when there is a diagnosis of a chronic, potentially debilitating condition, such as dementia, Alzheimer’s, Parkinson’s, or a major injury.

Crisis Planning occurs after an emergency often involving hospitalization. This could be a fall and fracture, a stroke, or a heart attack. The issue then becomes what type and level of care will be required after discharge.

Often, of course, the issue is money. The U.S. Department of Health and Human Services estimates that 70 percent of people over age 65 can expect, because of incapacity or disability, to need long-term care services at some point in their lives. The average cost for senior care in a skilled nursing facility is over $10,000 per person per month. How rapidly would that deplete your assets?

Starting January 1, 2026, California will reinstate asset limits for Medi-Cal’s non-MAGI programs. Individuals will be allowed to have up to $130,000 in assets, plus $65,000 for each additional household member. For married couples or registered domestic partners, the usual combined limit will be $195,000, unless spousal impoverishment rules apply, which set different limits.

These changes could significantly impact whether you qualify for assistance with long-term care. With nursing homes costing over $10,000 a month, how long would your savings really last under the new rules?

But the issues go well beyond money.

Pre-Planning for Elder Care: Estate Planning

Now let’s follow that journey of Ann, 80, who has two grown children, a daughter Jeanne and a son Steve. They all live in California.

Ann’s late husband, who passed away six months ago, was a Vietnam War veteran, which makes her what the Veterans’ Administration (VA) calls the “surviving spouse of a wartime vet.” Ann owns a $500,000 house and has savings of $130,000. Her sole sources of income are $2035 a month from Social Security and some interest from her savings—which she manages to stretch remarkably well, though her savings are slowly dwindling.

At 80, Ann is healthy and vigorous. Steve isn’t concerned about her health. But Ann’s more responsible daughter, Jeanne, knows better.

Realizing that her mother has done no pre-planning, and has no Will or Trust, Jeanne takes her mother to a qualified estate attorney at CunninghamLegal to create an Estate Plan. Generally, pre-planning and estate planning are one and the same. Estate planning is its own, complex topic, and I invite you to read our extensive article on estate planning by clicking here. But a brief summary may be helpful.

Generally, an estate plan involves establishing a Revocable Living Trust, which will help Ann and her heirs:

- Manage her assets during her lifetime.

- Avoid probate for her heirs, generally a long and messy process in the courts, running one to two years, during which her assets will be tied up after she dies.

- Minimize inheritance and other taxes.

“Revocable” simply means that Ann can change the terms of her Living Trust during her lifetime. She should review the content of her estate plan, including the Living Trust, every three years. Creating an estate plan isn’t a one-time event. It should be a habit.

Ann designates Jeanne as her Successor Trustee. Steve is designated Alternate Successor Trustee and would take over Jeanne’s responsibilities should she be unable to fulfill them.

A number of other documents get signed, along with the Living Trust. These are:

- A Pour-Over Will, which is a special type of Last Will & Testament that pairs with a Living Trust.

- A Durable Power of Attorney (DPA), which authorizes an individual, in this case Jeanne, to sign agreements on Ann’s behalf, and access her assets that are not in her Living Trust, such as an IRA, annuity, 401(k) or life insurance—should Ann become incapacitated. Jeanne receives Ann’s DPA, with Steve next in line should Jeanne be unable to carry out these duties. Without this Power of Attorney, should Ann be incapacitated, how could these assets that don’t go in a Living Trust be managed?

- An Advance Health Care Directive and/or “Living Will” giving Medical Power of Attorney to a Trustee authorized to make healthcare decisions for Ann when she becomes incapacitated. This includes specific directions about how Ann wishes to be cared for, including, to put it bluntly, when Ann wants doctors to “pull the plug” if she is on life-support systems. Jeanne found it surprisingly easy to have this conversation with Ann and her doctor at this non-crisis stage.

- A HIPAA Authorization, giving whoever has Medical Power of Attorney the right to access Ann’s confidential medical records.

- A Pre-Need plan with a funeral home and cemetery. Again, Jeanne finds that Ann is not reluctant to discuss such a plan so as not to leave the choices uncertain and her children at a loss. Ann requests that she be cremated and that her ashes be buried next to her late husband.

Working With an Attorney at CunninghamLegal to Plan for Elder Care

Jeanne enlists experienced elder law services from CunninghamLegal using qualified elder law attorneys throughout the planning process. Why? Because she needs answers to her elder law questions, and because she knows “she doesn’t know what she doesn’t know to ask” about the issues. For example, she’s surprised to learn that an IRA does not belong in a Trust. And she learns that her mother just has time to do a “Portability Election” on her husband’s estate tax exemption before the deadline passes. Without an attorney’s service, she would have no idea that these were serious concerns.

The qualified attorney at CunninghamLegal also tells Jeanne and Ann that pre-planning should also prepare for the next stage, non-crisis planning, by giving Jeanne, as Successor Trustee, so-called “Gifting Power,” the power to make gifts from Ann’s assets, if necessary. This can be vital to protect assets from the government when public assistance such as Medicaid has been received.

CunninghamLegal also says it’s wise to establish a game plan for the order in which assets should be liquidated if needed to pay for long-term care. In this case, the attorney also suggests Ann consider purchasing long-term care insurance, though she brings in an outside expert on insurance to advise her. Jeanne receives Ann’s “Gifting Power,” along with her Durable and Medical Powers of Attorney.

Non-Crisis Planning for When Elders Are No Longer Able to Care for Themselves

A couple of years go by. Ann has become increasingly frail and is beginning to show early signs of dementia. Her words often make no sense. Jeanne does not panic. Rather, she uses Ann’s Advance Healthcare Directive and HIPAA Authorization to interact directly with her mother’s physicians, as well as her Durable Power of Attorney to communicate with Ann’s lawyer at CunninghamLegal and her tax preparer.

Jeanne also begins arranging for some home-care services for her mother. Ann, like most people, wants to remain in her home even though she’s unable to care for herself. Jeanne finds it awkward that her mother refuses to acknowledge she has health issues needing care but realizes this is her way of retaining her dignity.

Jeanne is careful to ask Ann’s permission to access her accounts, which Ann readily grants. Jeanne takes over paying her mother’s bills and immediately realizes that Ann will probably outlive her money: her in-home care is $5000 a month and Ann’s social security income is only $2035. The average wage for an in-home aide is $20 per hour; if a licensed nurse is required, that increases considerably. Is she overpaying? Is there some other eldercare option or help from the government available? Help!

Should Ann’s dementia worsen and make her uncooperative or subject to undue influence by the scammers who often come out of the woodwork to prey on the elderly, Jeanne might also seek to become her mother’s Conservator.

Elder-Care Crisis Planning

Six months later, Ann falls and breaks her hip. She’s rushed to the hospital. Her doctors tell Jeanne that surgery for the broken hip is not an option, as Ann is 83 years old and has been diagnosed with dementia, which is often precipitated by physical trauma such as a fall.

The hospital stay runs more than $13,656 a day and is covered by Medicare. After three days, Ann is discharged and is sent to a rehabilitation facility. At this point, Medicare covers all expenses for up to twenty days. Then it restricts payment to $204 per day, but only so long as Ann has not “plateaued.” This means that Ann has to continue to get better for Medicare to continue paying. If she reaches a plateau, Medicare stops covering expenses.

There’s yet another restriction: no matter what the circumstances, Medicare will only pay for 100 days of rehab a year per benefit period. The clock on this can reset after a 60-day break in skilled care, not automatically every January 1st.

After thirty days, Ann is considered to have plateaued and is discharged from rehab. Her doctor tells Jeanne that it is extremely unlikely her mother will ever be able to return home. It’s time for crisis planning to move into high gear.

Step 1: Determine Level of Care

There are several levels of elder care available. These are, in order from least to most intensive and generally least to most expensive:

- In-home care: the patient returns home but has assistance.

- Assisted living: a facility where patients have some assistance but are generally capable of looking after most of their needs, such as preparing meals and cleaning.

- Board and care: which provides room and board as well as assistance as needed.

- Memory care: for dementia and Alzheimer’s patients who are capable of some self-care.

- Skilled nursing care: a facility in which most patient needs are taken care of by health-care professionals.

- Respiratory care in skilled nursing facility: which is extremely expensive, perhaps as high as $30,000 a month.

Medicare only covers a short time of skilled nursing care right after a hospital stay, and it doesn’t pay for most long-term elder care, which usually has to be paid for out of pocket. But starting January 1, 2026, California is bringing back limits on how much money and property you can have to qualify for Medi-Cal. For individuals, the limit will be $130,000, and for couples, it will be $195,000, with some extra allowances for other household members and protections for spouses. This means that older adults and people with disabilities who need help with long-term care might be able to get Medi-Cal if they meet these rules.

However, there is some limited needs-based public assistance available through Medicaid and the VA, which we’ll look at below.

Given her condition, Ann is transferred from the hospital to a skilled nursing facility, which costs $9,000 – $10,600 or more a month, a fairly typical amount.

Jeanne and her brother Steve carefully watch over the quality of the care at both the rehab center and skilled-nursing facility to guard against the possibility that elder abuse is taking place.

Step 2: Determine “Burn Rate”

It’s now up to Jeanne to determine Ann’s exact financial situation. Ann’s cost of skilled nursing care is $10,000 a month; her other living expenses run $500 monthly. Her social security income is $2035 a month. Her assets are now just $130,000 in savings and a half-million-dollar house.

Jeanne, after doing a few calculations, realizes that her mother will run out of money in about 14 months and 15 days. The average stay for permanent nursing-home residents is four years or forty-eight months. Where’s the rest of the money going to come from? Not from Medicare, which has paid all of Ann’s living expenses that it intends to.

Two public-assistance resources are the national Medicaid, which in California, where Ann lives, is known as Medi-Cal, and the VA. Let’s take a look at each.

Step 3: Understanding Medicaid (Medi-Cal) Elder-Care Benefits

Medicaid, which goes by “Medi-Cal” in California, “Access” in Arizona, and other names in other states, will only pay for elder care in a skilled nursing facility. It will not pay for assisted living or any other non-skilled nursing facility, such as a board and care. It very rarely pays for in-home care, and only under limited circumstances: some very limited waivers, as the Assisted Living Waiver (ALW) Program may provide for in-home care; but these programs have extensive waitlists.

For Ann to receive Medi-Cal, she must qualify both medically and financially. As a patient in a skilled-nursing facility with dementia and a broken hip that cannot be operated on, she clearly qualifies medically.

Financial qualification is more complex, and here’s where Jeanne again needs to consult elder law services of California at CunninghamLegal for professional advice. Let’s see how Medi-Cal planning could play out for Ann.

As of January 1, 2026, Medi-Cal will reinstate an “asset test.” However, an “income test” still exists when determining whether, and to what extent, Ann will receive a Medi-Cal benefit to help pay the monthly nursing home bill. This means that Ann could theoretically have up to $130,000 in assets and still qualify to receive Medi-Cal.

If the cost of the skilled nursing care facility is $10,000 per month, Ann must contribute $2,035 of her $2,035 Social Security payment per month as her “share of cost,” keeping $0 as a personal maintenance reserve. If Ann’s other income is $1,000 per month from a money market account, then Ann’s share of cost increases by $1,000 to $3,035 per month. Since the bill is $10,000 per month and Ann pays $3,035 per month, Medi-Cal pays the $7,000 difference directly to the skilled nursing care facility. However, if proper estate planning is in place, it is possible to keep the $1,000 per month and NOT pay it to the nursing home. With such proper estate planning, this $1,000 per month can be made “unavailable” to Ann and therefore not subject to Ann’s “share of cost” for Ann’s nursing home stay.

Instead of Jeanne continuing to pay the skilled-nursing facility out of her mother’s $130,000 savings and income of $1,000 until they’re gone, Jeanne could work with Ann’s estate attorney at CunninghamLegal and her CPA to work through possible solutions, including applying for Medi-Cal.

Jeanne works with Ann’s estate attorney at CunninghamLegal and her CPA to work through possible solutions, including applying for Medi-Cal. She definitely needs their expert estate and elder law services and advice—because as you will see, the strategies are complex and require serious legal help.

Step 4: Protecting Mom’s Assets During Her Disability, Including Her Home

Say Jeanne applied for Medi-Cal benefits for Ann. As we saw, under Medi-Cal regulations, which differ in other states, Ann would only be allowed to keep a limited amount of her income ($35) for her personal living expenses. Importantly, Jeanne works with her attorney at CunninghamLegal on how to properly leverage her income and assets to maximize her quality of life within these requirements.

But there’s another catch here. Medi-Cal is authorized to recover the amounts it pays to an individual aged 55 or older, or for skilled nursing facility care at any age, from the recipient’s estate. This includes Ann’s home if it were to go through probate after Anne’s death.

Fortunately, because Ann has created a Living Trust and transferred her home to it, there is no reimbursement at Ann’s death. Jeanne and her brother Steve can inherit the house and not have to repay Medi-Cal. But please note: this is a complex undertaking which requires the work of a qualified attorney experienced with these issues under California law. Set up a call with CunninghamLegal to learn more.

Step 5: Possible Use of Veterans’ Administration (VA) Aid & Attendance Benefits

Here’s another important Medicaid requirement to keep in mind: if a Medicaid recipient might receive VA benefits, they’re required to apply for them. And that’s what Jeanne is required to do on Ann’s behalf. As the “surviving spouse of a wartime veteran” who has not remarried, Ann applies for Veterans’ Administration Aid and Attendance benefits. These VA elder care benefits are basically the same as the elder care benefits also awarded to both disabled and wartime veterans.

Ann isn’t required to give up her home to receive these benefits. In fact, VA benefits, unlike Medicaid/Medi-Cal, can be used for in-home care—a huge advantage.

However, to receive these benefits, Ann’s medical expenses must exceed her income, and Jeanne must “spend down” her mother’s other asset, her $300,000 savings, to a maximum of $ $158,779 (as of 2025. A CunninghamLegal attorney may also be able to transfer all or part of these assets into an irrevocable trust for Ann’s children–but again this must be done properly, and usually in stages.

Ann is awarded benefits of $ 1,258 per month—the typical amount is anywhere from $ 1,000 to $ 3,000. This comes in the form of a check that Jeanne can use to pay any of Ann’s expenses.

Step 6: Deciding About Long-Term Care Insurance

Ann does not have long-term care insurance, which might have changed the equation considerably. Here at CunninghamLegal, we believe everyone should at least consider long-term care insurance. I’m going to pause the tale of Ann to offer some summary information now, but this is a complex topic, and you may wish to view our webinar on the pros and cons of long-term care insurance.

Most importantly, the policy must be purchased before it is needed. Fortunately, there are some carriers who allow policies to be purchased up until the time the Insured turns eighty-five! However, if there’s a dementia, Alzheimer’s, or Parkinson’s diagnosis, you’ll probably be denied coverage. If you do get coverage, there will most likely be a ninety-day waiting period before it can be used.

Formerly, purchasing the insurance required a premium of, say, $500-$700 per month—every month from the time the coverage was purchased. If it wasn’t necessary to use the coverage, these payments were forfeited. “Use it or lose it.”

Today, you can purchase the insurance for a flat rate of say $100,000-$120,000 which can provide up to about $300,000 to $350,000 in overall coverage. However, if it turns out that the coverage is unnecessary, the Beneficiary’s heirs will receive the $ 100,000 to $120,000 up-front payment back, plus interest. “Use it or lose it” no longer applies.

Not all policies are created equal. Some long-term care insurance, like VA coverage, allows the Insured to receive in-home care, if desired, and doesn’t require transfer to a skilled nursing-care facility. Some offer partial coverage, which may be perfectly acceptable. Also, bear in mind that 80 percent of those admitted to long-term care skilled-nursing facilities leave within 120 days, so a policy restricted to skilled-nursing facilities may not cover all long-term care needs.

Again, long-term care insurance is an important aspect of elder-care planning that we suggest everyone consider thoughtfully. From personal experience, we can say that having long-term care insurance often makes life considerably less stressful for other family members, especially those with Durable or Medical Power of Attorney.

Is long-term care insurance worth it? Like most investments, “it depends” and you should seek expert, independent advice on your particular situation.

Where Does the Money for Elder-Care Typically Come From?

As I mentioned earlier, U.S. Department of Health and Human Services (HHS) estimates that 70 percent of people over age 65 can expect to need long-term care services at some point in their lives. According to the latest available figures from the Centers for Disease Control (CDC), some 1.4 million adults now live in skilled nursing facilities. Another 4.8 million remain in their own homes but get personal-care assistance.

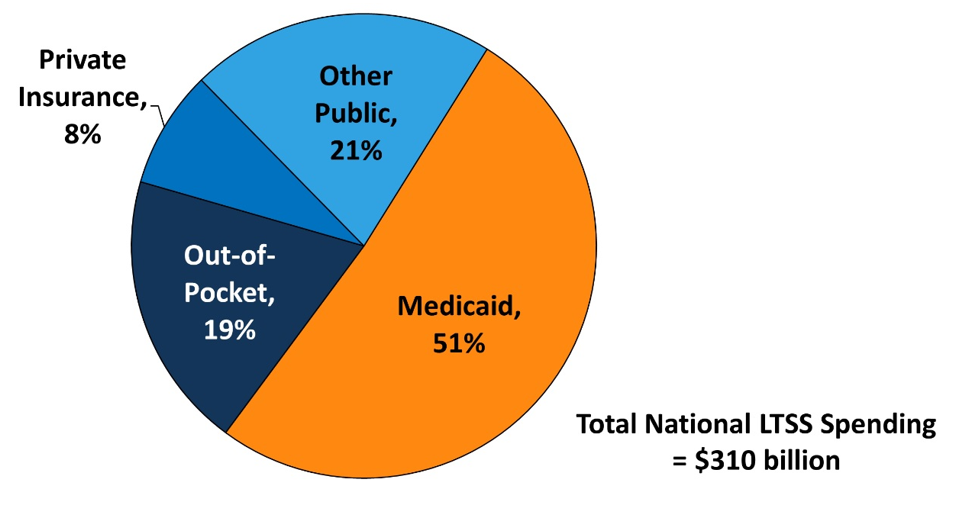

Who Pays For Long-Term Care?

As you can see, Medicare covers only a small portion of long-term care expenses. Medicaid accounts for the largest share, while out-of-pocket costs still make up a significant portion of the total.

With careful planning, Jeanne managed to bring that percentage way down. Let’s see how it played out.

Ann’s Last Years – Well-Planned and Controlled

Ann lived another three years with her dementia, until she finally passed from a stroke at age 86. Jeanne got to hold her hand and was by her side at the last.

Since the VA did not cover all Ann’s expenses, Jeanne applied for and received Medi-Cal assistance on her mother’s behalf to cover the shortfall. Before applying, and when Ann still had mental capacity, they put Ann’s house in a revocable trust naming Jeanne and her brother Steve as Beneficiaries. When Ann passed, the State of California couldn’t seize it to recover Ann’s substantial Medi-Cal bills.

An Irrevocable Trust held Ann’s $130,000 remaining savings. Jeanne and Steve split this, as well as the proceeds from their sale of their mother’s house.

Jeanne Practiced Self-Care, Too

Jeanne found herself under sometimes considerable stress during those final years, but with her attorney, financial advisor, and CPA by her side, she made the right moves.

Jeanne also learned she needed to take care of herself as well as her mother. When burn-out threatened to set in, she asked her brother Steve to step up and pitch in. Although he was reluctant at first, Jeanne pointed out that not only was Ann his mother, but he was a 50 percent Beneficiary in Ann’s Trusts and Will.

Steve agreed to help out, saving Jeanne from the burn-out that family caregivers often go through. When all was said and done, he even thanked his sister for her great work, and the siblings became closer than they had been since childhood.

What Do We Do?

The lawyers and staff at CunninghamLegal help people plan for some of the most difficult times in their lives; then we guide them when those times come. We can help families like Ann, Jeanne, and Steve at any point in the Elder Care journey—but we can help most when we’re involved in planning before a crisis occurs.

Make an appointment to meet with CunninghamLegal for Estate Planning, Medi-Cal, Trust Administration, Tax Planning, and elder law services of California. We have offices throughout California, and we offer in-person, phone, and Zoom appointments. Just call (866) 988-3956 or book an appointment online.

Please also consider joining one of our free online Estate Planning Webinars.

And here are some webinars specifically on long-term care and elder-law issues.

We look forward to working with you!

Best, Jim

James L. Cunningham Jr., Esq.

Founder and CEO, CunninghamLegal

We guide savvy, caring families in the protection and transfer of multi-generational wealth.